This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sustainable investing assets in the United States have plunged by more than half to US$8.4 trillion at the end of 2021 from US$17.1 trillion at the end of 2019, according to a new report from the US Forum for Sustainable and Responsible Investment (US SIF). Portfolios classified as responsible investments dropped to $3.0

Notably, North America has declined significantly in its representation in the global sustainable bond market, with volumes of $124 billion in 2024 already having declined nearly 30% from 2021. Global focus on sustainable development and investment will support the market.

These new rules, intended to counteract greenwashing, spell out the criteria for a greeninvestment and require market participants to disclose how they are aligned with them. The outcome is a seamless approach to customized sustainable investing. For more information, visit www.impact-cubed.com/regulatory solutions.

Adopted in 2021 and coming into effect for the 2024 financial year, the CSRD is the regulatory framework requiring firms to file social and environmental data and impact reports. Here are the main rollbacks proposed in the initial package. But Maria van der Heide, head of EU policy at ShareAction, a U.K.-based

According to a 2021 OECD report , nature-related dependencies, impacts and risks are poorly understood and almost entirely uncompensated for in the financial sector. We need to encourage more targeted investments in nature-positive solutions that reverse biodiversity loss.

Investors have been in limbo for six months about the future of the regulation, which provides guidelines on the disclosures required of greeninvestment vehicles. Proxy categorisation system Introduced in 2021, SFDR was initially intended as a transparency regime imposing disclosure requirements for fund managers.

Asset managers decide to re-label existing funds as greeninvestment vehicles for two reasons, according to Paul Lacroix, Head of Structuring at Smart Beta specialist investment firm Ossiam, an affiliate of Natixis. The first is client demand for investment solutions that are ESG-based,” he tells ESG Investor.

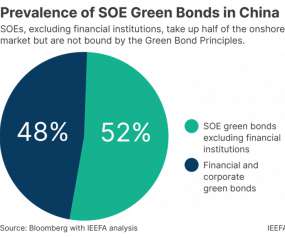

Inclusion of coal in green taxonomy would border on state-sanctioned greenwashing, says Christina Ng, Research & Stakeholder Engagement Leader, Debt Markets, and Putra Adhiguana, Energy Technologies Research Lead, Asia, at IEEFA. Its current green taxonomy excludes gas, liquefied natural gas and coal-fired power activities.

It was supported by an informal technical expert group, and a founding partner group consisting of Global Canopy, UNDP, UNEP FI, and WWF, to develop recommendations for more effective nature-related disclosures in order to promote more informed investment decision-making.

A key amendment requires 100% of the proceeds to fund green projects, instead of 50-70% previously. This is a big step for foreign investors who are eager to invest in China’s domestic green bond market but have concerns about greenwashing—inadvertently buying ‘green’ bonds that, in fact, support non-green projects.

In previous years, AIGCC found that investors were relying on third-party ESG data service providers and other globally available standards such as the EU Taxonomy to define net zero, low carbon or climate aligned investments. The situation looks to be improving as it was cited by 56% of respondents in 2020, falling to 45% in 2021.

Having launched its framework in November 2022, the TPT aims to finalise its disclosure framework and implementation guidance and will develop sectoral guidance.

This split in opinion was showcased in a Morningstar Sustainalytics survey , in which 50% of respondents said they would like to see Article 8 and Article 9 categories replaced by labels, while 39% would prefer to keep Article 8 and Article 9 categories.

The case for more dynamic, quality green bond issuances The last UK green financing strategy expected that green gilts would “help catalyse further growth of the corporate green bond market in the UK” – this appears under-delivered. This should crucially set a best practice to guide corporate markets.

This not only creates considerable confusion among investors but exposes them to accusations of greenwashing, as well as the risk of holding investments that are not aligned with their own ESD/SDG requirements. What is beyond doubt however, is that the ‘green’ label helps to attract significant asset flows.

trillion in 2021. Currently, there is no clear definition of what constitutes a “green” investment, which has led to a proliferation of green bonds that are not truly environmentally friendly.” ChinaSIF estimates that the size of China’s ESG market in 2022 was RMB 24.6 trillion (US$3.57 trillion) growing from RMB 18.4

The year started optimistically, fresh off the bold and ambitious agreement in November 2021 that established the Glasgow Financial Alliance for Net Zero (GFANZ). banks accounted for nine of the 12 largest financiers to the fossil industry in 2021, according to Banking on Climate Chaos , a report published in 2022 by BankTrack.

Not only does it echo an Australian ruling from 2021 which ruled that governments have a duty of care to protect young people from the impacts of climate change. The act also kickstarted an era of greeninvestment competition.

companies rose sharply between 2021 and 2024, although overall support was 27% in 2024, down from 37% in 2021. But these dropped precipitously starting in 2022, when central banks ramped up interest rates, the Ukraine war drove up energy prices, and Europe established more stringent anti-greenwash fund-disclosure rules.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content