This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The European Commissions DG FISMA has emphasised the merits of replacing the Sustainable Finance Disclosure Regulations (SFDR) existing Article 8 and Article 9 labels with formal categories based on clearer criteria.

Even if we quickly agree on disclosure frameworks and measurements around biodiversity, disclosures that are voluntary and not supported by regulation are vulnerable to greenwashing which is widespread in the ESG space. We need to encourage more targeted investments in nature-positive solutions that reverse biodiversity loss.

Asset managers decide to re-label existing funds as greeninvestment vehicles for two reasons, according to Paul Lacroix, Head of Structuring at Smart Beta specialist investment firm Ossiam, an affiliate of Natixis. The first is client demand for investment solutions that are ESG-based,” he tells ESG Investor.

European regulators have ratcheted up efforts to eliminate greenwashing from the investment sector. End of an era I – The fight against greenwashing inched ahead with the release of final guidelines for naming ESG- or sustainability-related funds by the European Securities and Markets Authority (ESMA).

Dutch firm’s fifth impact-focused investment strategy launches amid continued demand for Article 9 funds. ING Asset Management’s new SDG Impact Strategy will provide clients with exposure to companies that contribute specifically to the 17 UN Sustainable Development Goals (SDGs), responding to strong demand for ‘dark green’ investments.

Inclusion of coal in green taxonomy would border on state-sanctioned greenwashing, says Christina Ng, Research & Stakeholder Engagement Leader, Debt Markets, and Putra Adhiguana, Energy Technologies Research Lead, Asia, at IEEFA. This article was co-authored by Putra Adhiguna , Energy Technologies Research Lead, Asia, at IEEFA.

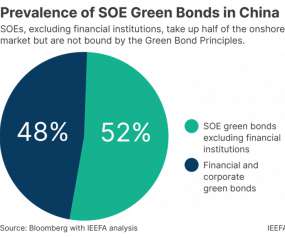

A key amendment requires 100% of the proceeds to fund green projects, instead of 50-70% previously. This is a big step for foreign investors who are eager to invest in China’s domestic green bond market but have concerns about greenwashing—inadvertently buying ‘green’ bonds that, in fact, support non-green projects.

This article first appeared in Forbes. There have been bad faith actors from the corporate world, greenwashing their activities, depleting the world’s resources, damaging the environment and wasting the planet’s and the climate movement’s time and energies. It serves none of our goals to persist in old tropes of goodies and baddies.

This sparked a plethora of comment this week warning of investor confusion and the prospect of a rethink among those SFDR Article 9 funds that downgraded over the past six months for fear of being accused by regulators of greenwashing. To quote a past contributor to ESG Investor , for fund managers, it’s still not easy being green.

In her confirmation hearing on Wednesday, Albuquerque expressed her position that the EU’s Sustainable Finance Disclosure Regulation (SFDR) could more effectively address greenwashing risk with the introduction of a labelling regime that communicated clearly the sustainability attributes of investment products.

I’ve long been interested in climate action, and as I’ve become more interested in investing, I’ve become totally passionate about how to do sustainable investment RIGHT – or at least BETTER. In my last article about learning to invest sustainably, I wrote that it’s hard to find funds that truly align with my green sensibilities.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content