This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

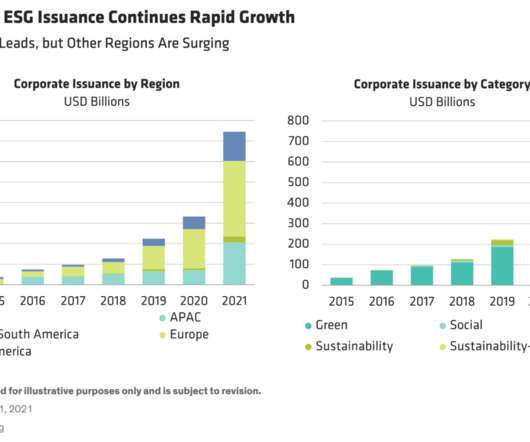

ESG-labeled bond issuance surged to new heights in 2021. Greenbonds, which fund particular projects, continued to dominate. But issuance of social, sustainability and sustainability-linked bonds—which reference specific key performance indicators, or KPIs—grew fastest (Display). Location: London.

The Government of India will issue its first-ever greenbond this month, according to an announcement by the Reserve Bank of India, with plans to raise approximately US$2 billion to support green infrastructure projects aimed at reducing the carbon intensity of the economy.

Deutsche Bank announced today that it has raised €500 million through its first-ever socialbond offering, with proceeds aimed at supporting the bank’ssustainable asset pool which provides financing for areas including affordable housing, and access to essential services for elderly or vulnerable people.

Asset managers Head of Fixed Income hopes market expansion will eliminate need for the purely greenbond-focused vehicle within the next decade. Niche to mainstream evolution Storebrand stated that the fund was the first commercial greenbond fund, building on the first ever greenbond issued by the World Bank in 2008.

Sustainablebond issuance outperformed the broader market in the second quarter of 2022, reaching a record 15% of global total issuance, according to a new report from Moody’s ESG Solutions. Moody’s maintained its forecast for stronger GSSS volumes in the second half of the year, and its $1 trillion full year estimate.

Indeed, sustainable investments are key to building a society that is low-emission , keeping global warming below 2°, and socially inclusive. An interesting ongoing trend is the growth of greenbonds. In 2022, greenbond issues accounted for more than half of all sustainablebonds issued in the same year (58%, $487.1

Shades of Green’s Second Party Opinions (SPOs) are independent, research-based assessments on companies’ and governments’ green, sustainability and sustainability-linked debt issuances and frameworks, evaluating alignment with market standards, typically provided before any borrowing is raised. trillion 2 years ago.

The European Central Bank (ECB) announced today the publication of a series of new statistical indicators aimed at helping to analyze climate-related risks in the financial sector and track the progress of the sustainable finance market.

Green, social, sustainability, sustainability-linked and transition ( GSS+ ) bonds are shaking off recent macroeconomic and geopolitical volatility, with the market on track to hit US$5 trillion in combined issuance by the end of the year. Greenbonds made up 62% of the total aligned GSS+ debt (US$278.8

For the report, Sustainable Fitch examined the green, social, sustainability and sustainability-linked labeled bonds rated by its ESG Ratings service, with a focus on the instruments’ Use of Proceeds’ contribution to green and social impact, and the level of transparency and ambition in project or target selection.

Ujala Qadir, Director of Strategic Programmes at the Climate Bonds Initiative, explains why the organisation has expanded its greenbond taxonomy to cover climate resilience. The market has matured as investors, issuers and other market participants have become more familiar with labelled debt,” she told ESG Investor.

Despite development barriers, opportunities are emerging for investment in sustainable assets in growing market. Africa has seen rapid growth in issuance of green, social, sustainability and sustainability-linked (GSS+) bonds and could prove enticing to investors, in spite of existing challenges.

Achieving net zero by 2050 could require the climate bond universe to reach US$36 trillion by 2025 and over US$60 trillion by 2030, it added. The ESG-labelled bond markets are typically considered to include green, social, sustainability, sustainability-linked and transition bonds.

Sovereigns have been relatively late entrants to sustainablebond markets following corporates and supra-national entities (such as the World Bank and the European Bank for Reconstruction and Development), which issued the first green debt securities in the mid-2000s.

Our sustainable debt markets are designed to highlight sustainable investment opportunities to investors with a green, social or sustainable investment agenda. The number of sustainable debt instruments listed on Nasdaq grew by 11% during 2022 and the volume of listed bonds grew by 27%.

The Asian Development Bank (ADB), which estimates a US$3.1 Global sustainablebond issuance surged in 2021, with data providers estimating total volumes just above or below US$1 trillion; greenbonds accounted for roughly half. Developing economies globally need to invest as much as US$4.5

An important key to unlocking that finance lies in green and sustainable emerging market bonds, which promise lenders both returns and the opportunity to invest in projects with an ESG impact. trillion by September, with demand for emerging market labelled bonds far outstripping the rest of the world.

Standardising environmental and social impacts in land-use investments needs to be a priority for the financial sector. Banks and other financial intuitions (FIs) have the potential to help transition land-use to become ‘nature positive’ in addition to ‘net zero’, by redirecting investment to sustainable land-use projects.

Second-quarter issuance represented US$238 billion, down 20% year-on-year, while global issuance of green, social, sustainability, sustainability-linked and transition bonds totalled US$238 billion – also down 20%. The EV GreenBond originated from the group’s asset finance arm – Lombard.

After years of debate, the European Union GreenBond Standard (EUGBS) finally made its formal debut at the end of last year. However, all of the projects must comply with the taxonomys do no significant harm (DNSH) criteria, as well as be certified by a designated EU greenbond reviewer.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content