This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Pandemic bonds join a growing list of sustainability-linked financial instruments that have been gaining the attention of investors worldwide. The bonds alone come in a veritable rainbow of flavors: greenbonds; climate bonds; sustainability bonds; social bonds; ESG bonds; blue bonds (related to oceans); and more.

(“O-I Glass”, “O-I” or the “Company”) announced that the Company has completed full allocation of the proceeds from its second round of GreenBond offerings to advance the company’s climate-change strategy. launched private GreenBond offerings of $690 million and €600 million, respectively. and OI European Group B.V.

In fact, completeness and quality of information, definition of the methodologies used to process it, and clarity in communication are required. Transparency is becoming a pre-requisite.

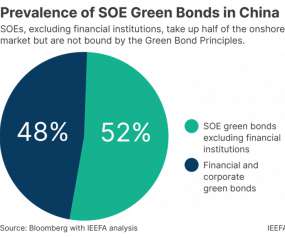

The IEEFA’s Christina Ng says China’s state-owned enterprises continue to allocate up to half of their greenbond proceeds to non-green projects. . China’s ambition to green its financial market has been making significant progress. SOEs accounted for about half the onshore green issuances from 2019 to 2022.

It is definitely something I will keep my eyes on. The current greenbonds used to offset GHG emissions can be expanded to identify a roadmap that supports individuals within a corporation’s community or supply chain. There was also a lot of talk on incorporating ESG in emerging markets, and I completely agree with that.

Attitudes towards the place of nuclear power in sustainable finance markets have "definitely shifted" in the last couple of years, an Environmental Finance event has heard - but their place in greenbonds remains a "separation point" in the market.

1 Seventy percent of investors in full- or part-time jobs would probably or definitely include sustainable funds in their 401(k)s if offered by their employers’ plans. Investors can expect to see more sustainable efforts like the Principal bond: The sustainable bonds and loans sector is experiencing record-breaking growth.

19, Fifth Third Bancorp announced a definitive agreement to acquire Dividend Finance, a leading fintech point-of-sale lender, providing financing solutions for residential renewable energy and sustainability-focused home improvement. 1, 2021, Fifth Third Bancorp settled the issuance of its inaugural GreenBond for $500 million.

Under this definition, products that are aimed at reducing ESG risk, without pursuing a specific sustainability goal, will not qualify for a sustainable label. Click here to access the greenwashing position paper and the sustainable finance report.

That’s a monstrous opportunity, and it broadens the definition of "sustainable finance" even further to include vast pools of capital to take on humanity’s most pressing challenges. We’ll focus, as my learning journey did, primarily on ESG investing and greenbonds and loans.

The GFTF is co-chaired by Gillian Tan, recently appointed as Chief Sustainability Officer of MAS, and Dr Ma Jun, Chair of the China Green Finance Committee, and is comprised of senior representatives and sustainable finance experts from financial institutions and green FinTech companies from Singapore and China.

Several of these funds also tackle broader social and environmental themes alongside the energy transition, which has led to inconsistent definitions and approaches across strategies.

Financial institutions and market participants will be able to refer to a common set of definitions under the CGT to facilitate sustainable development in markets covered by the CGT. This includes the basis for identifying, selecting, managing, and reporting on expenditures financed with greenbonds. degree celsius (1.5°C)

The document also includes recommendations aimed at establishing the EU Taxonomy as the sole reference point to be used to assess and measure sustainability performance, noting that the SFDR – which predates the Taxonomy – provides its own, more flexible, definition of sustainable investments.

Mandatory EU GreenBond Standard risks slowing issuance, but voluntary approach can still drive Taxonomy-aligned volumes. On the face of it, the market for greenbonds is heading in the right direction, and fast.

In ESMA’s new report, the regulator noted that while a clear framework or definition for transition funds does not yet exist, these funds already appear to be taking a homogeneous investment approach, with a much higher degree of similarity relative to green funds.

Actions will include the definition of metrics and strategy approaches, encompassing engagement, data-driven research and monitoring, and increasing climate-finance exposures.

Gas projects were not widely backed by these bonds. And as debate continues about whether sustainable or greenbond instruments offer any borrowing cost advantage over conventional debt, a recent study found that they can – by up to eight basis points in fact.

Last year, new issuance of GSS bonds as defined by PwC totalled €500 billion, which accounted for approximately 13.7% PwC does not include in its GSS definitionbonds that are not directly tied to specific sustainability projects. Social bonds are expected to make up 23% and sustainable bonds 28%.

Up until now, many ESG analyses have focused primarily on environmental risks and impacts, particularly as issuance has predominately been skewed towards Greenbonds. However, with the rise of sustainability-linked bonds, a wider and more comprehensive view is becoming increasingly important.

What Is Green Finance and Why Does it Matter so Much? What is green finance? There are a lot of questions and doubts about its definition. What countries are the best for green finance? What is green finance? How does it differentiate from sustainable finance? Let’s try to clear up some of the confusion.

19, Fifth Third Bancorp announced a definitive agreement to acquire Dividend Finance, a leading fintech point-of-sale lender, providing financing solutions for residential renewable energy and sustainability-focused home improvement. 1, 2021, Fifth Third Bancorp settled the issuance of its inaugural GreenBond for $500 million.

trillion in Asia-Pacific alone; regulatory uncertainty around a concept barely a decade old and the difficulty of valuing a communal fluid asset has opened a trench in financing between sustainable greenbonds and their blue peers. The cumulative value of greenbonds issued reached US$2.2

Initial reactions suggested the market has welcomed some aspects – such as definitions for what could be included in a fund with an ‘impact’ or ‘transition’ label – but is baffled by others. Italy’s green debt relief – Scarcity of sustainable assets was only one of the reasons for record-breaking demand for €9 billion (US$9.71

“The issuer base is likely to expand through multilateral support and as investor appetite for sustainable bonds catches up with vanilla bonds,” Moody’s added. Global sustainable bond issuance surged in 2021, with data providers estimating total volumes just above or below US$1 trillion; greenbonds accounted for roughly half.

The EU Green Taxonomy is also instrumental for the upcoming EU GreenBonds Standard. As the cornerstone of many current and upcoming regulations, the quality and comparability of the EU Green Taxonomy’s reporting data is crucial.

These include new definitions for green securitisation, a climate transition finance methodologies registry, new metrics for impact reporting, updated high-level mapping to the United Nations Sustainable Development Goals (SDGs), and pre-issuance checklists for greenbonds. .

Global interoperability To enhance interoperability with global taxonomies, MAS has commenced an exercise to map the Singapore-Asia Taxonomy to the IPSF’s (International Platform for Sustainable Finance) Common Ground Taxonomy (CGT), which currently covers the EU Taxonomy and China’s GreenBond Endorsed Project Catalogue.

So it’s definitely worth asking whether your funds are being managed with climate risk in mind. Greenbond funds invest in bonds that finance projects that facilitate the clean energy transition. Examples include Calvert GreenBond ( CGAFX ), Fidelity Environmental Bond ( FFEBX ), and Pimco Climate Bond ( PCEIX ).

Although China – through the GreenBond Endorsed Projects Catalogue – Hong Kong, Singapore and Thailand all exclude gas financing, most Asian taxonomies are more permissive in that regard. “In contrast, Malaysia and the Philippines follow a principles-based taxonomy that avoids using quantitative criteria.

Although China – through the GreenBond Endorsed Projects Catalogue – Hong Kong, Singapore and Thailand all exclude gas financing, most Asian taxonomies are more permissive in that regard. “In contrast, Malaysia and the Philippines follow a principles-based taxonomy that avoids using quantitative criteria.

China’s greenbond issuances are set to exceed US$100 billion this year, according to S&P Global Market Intelligence. The issuance of Chinese green debt, including instruments that meet only local standards, could grow by at least 80% this year after raising US$94.77 of the total amount of greenbonds issued.

Sherry Madera, Chair of FoSDA, says that the EU has been a leader in pushing the growth of taxonomies worldwide, but notes its own taxonomy was the preceded by the Chinese GreenBond Endorsed Projects Catalogue , and notes that its efficacy is yet to be tested. “It The limits of harmonisation.

Additional clarifications about the definition of a sustainable investment and about Article 8 and Article 9 classifications are expected soon, but in the meantime, caution and thorough due diligence remains key,” said Hortense Bioy, Global Director of Sustainable Research at Morningstar. Lack of definition.

For this to occur, greendefinitions, like the new criteria being developed by CBI, are required to facilitate financial flows to companies that can demonstrate their contribution to the transition of the agri-food sector. .

“Systemic reform, rather than individual announcements, is needed if we are to collectively mobilise the scale of investment needed for a just transition to a low-carbon economy.” The new €4 billion commitment adds to the €26.7

So there is a definite link between ESG ratings and data as they exist today and the broader idea of impact. Sustainable Business Went Mainstream in 2021 This is due, in no small part, to the explosion of ESG into the mainstream. The message is that managing climate and other ESG issues is core to business value,” Wintston writes.

For the report, EFAMA conducted an analysis of Morningstar Direct’s database, containing funds available to both retail and institutional investors, and relied on Morningstar’s definition of sustainable bond funds as those which explicitly indicate use of sustainability, impact, or ESG strategy in their prospectus or offering documents.

Alignment between JETP countries’ standards and definitions is also necessary to instil private investors with more confidence in prospective JETP-aligned investments, according to CoEPB’s Hillis.

A statement from 150 global financial institutions with US$24 trillion in AUM backed a “robust” GBF that provided a clear mandate for the alignment of financial flows, supported the disclosure of nature-related risks, impacts and dependencies, and outlined clear targets and definitions to enable the development of nature-positive projects.

Currently, there is no clear definition of what constitutes a “green” investment, which has led to a proliferation of greenbonds that are not truly environmentally friendly.” Hewett says a key challenge for China’s sustainable finance sector is a lack of unified standards and regulations.

She argued that because there is no standardized definition for sustainable investment, it is harder to determine which ESG initiatives are causing a net change for the good. Right now] ESG is basically a box of chocolates; you don’t know what you are going to get,” said Pretorius.

It is definitely going to be the case that there will be investor pressure and, indeed, a lot of incentives for companies that are looking to raise capital for their [green] transition efforts to continue reporting against the taxonomy, irrespective of whether theyre in scope, said the IIGCCs Donnachie.

To create it, investors must provide clear definitions of what qualifies as “impact investing” — along with easily understood social impact matrices that clarify the impacts they’re targeting, and their plan for pursuing them through their interactions with philanthropic partners.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content