This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The EU Green Taxonomy is also instrumental for the upcoming EU GreenBonds Standard. As the cornerstone of many current and upcoming regulations, the quality and comparability of the EU Green Taxonomy’s reporting data is crucial.

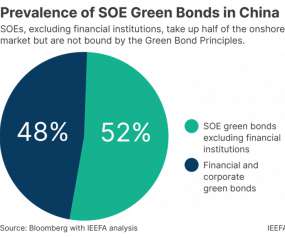

The IEEFA’s Christina Ng says China’s state-owned enterprises continue to allocate up to half of their greenbond proceeds to non-green projects. . China’s ambition to green its financial market has been making significant progress. SOEs accounted for about half the onshore green issuances from 2019 to 2022.

It had previously been possible to launch an EU environmental opportunities fund, claiming Article 8 classification under the Sustainable Finance Disclosure Regulation (SFDR) , while allocating as little as 10% of assets to demonstrably greeninvestments.

In ESMA’s new report, the regulator noted that while a clear framework or definition for transition funds does not yet exist, these funds already appear to be taking a homogeneous investment approach, with a much higher degree of similarity relative to green funds.

The rise of taxonomies of sustainable activities reflects a recognition from policymakers that global financial markets depend on a shared classification system if they are to identify ‘green’ investment opportunities. It is the lack of clear definitions that is slowing progress [in agreeing taxonomies].”.

Currently, there is no clear definition of what constitutes a “green” investment, which has led to a proliferation of greenbonds that are not truly environmentally friendly.” Hewett says a key challenge for China’s sustainable finance sector is a lack of unified standards and regulations.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content