This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Financial products and funds labelled as ‘sustainable,’ green,’ or ‘ESG’ on Swiss financial markets will be required to align or contribute to specific sustainability goals, with providers required to disclose how they intend to achieve the goals, according to new proposed rules unveiled by the Swiss Federal Council.

The EU Green Taxonomy was designed to accelerate the flow of money into green companies and projects, while simultaneously protecting investors from greenwashing accusations. The EU Green Taxonomy is also instrumental for the upcoming EU GreenBonds Standard.

As a result, much of the criticism stems from a mismatch between what a critic thinks sustainable investing is or should be about and how it is actually being practiced, often leading to claims of “greenwashing.” So there is a definite link between ESG ratings and data as they exist today and the broader idea of impact.

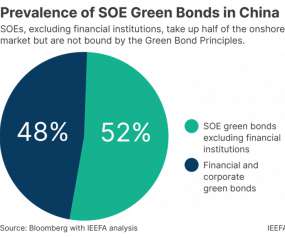

The IEEFA’s Christina Ng says China’s state-owned enterprises continue to allocate up to half of their greenbond proceeds to non-green projects. . China’s ambition to green its financial market has been making significant progress. SOEs accounted for about half the onshore green issuances from 2019 to 2022.

This market boom and increasing focus on labelled bonds represent a significant challenge for investors, where issues around information and behaviours have led to controversy, adverse headlines and even sanctions, along with widespread concerns around greenwashing. Identifying and avoiding greenwashing. Access Report.

Several of these funds also tackle broader social and environmental themes alongside the energy transition, which has led to inconsistent definitions and approaches across strategies. Nor will the fund channel transition capital to where it’s most needed – such as emerging markets firms.

European regulators have ratcheted up efforts to eliminate greenwashing from the investment sector. End of an era I – The fight against greenwashing inched ahead with the release of final guidelines for naming ESG- or sustainability-related funds by the European Securities and Markets Authority (ESMA).

“The issuer base is likely to expand through multilateral support and as investor appetite for sustainable bonds catches up with vanilla bonds,” Moody’s added. Global sustainable bond issuance surged in 2021, with data providers estimating total volumes just above or below US$1 trillion; greenbonds accounted for roughly half.

Financial institutions and market participants will be able to refer to a common set of definitions under the CGT to facilitate sustainable development in markets covered by the CGT. The proposed guidance is designed to help firms better understand the FCA’s expectations under the anti-greenwashing rule and other associated requirements.

“Understandably, being the first movers in the market, there is nervousness and caution amongst [JETP] stakeholders to get it right. “Investors face heightened concerns on the credibility of these transactions and potential greenwashing criticisms,” she says.

Although the EU Taxonomy and SFDR were designed to increase transparency and reduce opportunities for greenwashing, it’s still early days, and there is much work to do. Lack of definition. It is also forcing some funds to downgrade their claims and status. Asset managers should explain which PAIs they consider and why,” added Bioy.

The document also includes recommendations aimed at establishing the EU Taxonomy as the sole reference point to be used to assess and measure sustainability performance, noting that the SFDR – which predates the Taxonomy – provides its own, more flexible, definition of sustainable investments.

No country in the region has made reporting against the frameworks mandatory, further increasing greenwashing risk and due diligence costs. A comprehensive taxonomy can mitigate the risk of greenwashing by enforcing stringent requirements and maintaining transparency.” It should also mandate compliance and reporting.

No country in the region has made reporting against the frameworks mandatory, further increasing greenwashing risk and due diligence costs. A comprehensive taxonomy can mitigate the risk of greenwashing by enforcing stringent requirements and maintaining transparency.” It should also mandate compliance and reporting.

Mandatory EU GreenBond Standard risks slowing issuance, but voluntary approach can still drive Taxonomy-aligned volumes. On the face of it, the market for greenbonds is heading in the right direction, and fast.

The goal should be to ensure that asset managers have all the data needed to fulfil regulatory requirements by aligning with the taxonomy and to ensure that investors are investing in sustainable funds validated by regulators and avoiding greenwashing,” she said.

In a sector where greenwashing is an increasingly common problem, and practically anything can be presented as an impact investment regardless of the business’ actual impact, this transparency is important. Such incentives ensure accountability and a focus on delivering measurable social impact alongside financial returns.

Currently, there is no clear definition of what constitutes a “green” investment, which has led to a proliferation of greenbonds that are not truly environmentally friendly.” ChinaSIF estimates that the size of China’s ESG market in 2022 was RMB 24.6 trillion (US$3.57 trillion) growing from RMB 18.4 trillion in 2021.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content