This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As the COP28 meeting begins and the world looks to the financial sector to step up on the climate crisis, the global sustainable investment industry is finally coming to grips with allegations of greenwashing that have plagued it for years. Under the new definitions in 2022, those assets are 14% lower at US$30.3

Chinese asset managers are improving ESG awareness, but weak regulation means green claims often don’t match reality, says Greenpeace. Greenwashing is a growing risk in the Chinese fund management sector, as marketing of ESG products runs ahead of standards and regulatory oversight, a new report by Greenpeace has found.

Investors have been in limbo for six months about the future of the regulation, which provides guidelines on the disclosures required of greeninvestment vehicles.

Meanwhile, most people – 79% overall and 90% of investors under age 45 – say they want to invest in socially and environmentally friendly ways. Even if they’re not actively greenwashing, most companies don’t publish information about their emissions or other environmental impacts. And more importantly, what can we do to bridge it?

European regulators have ratcheted up efforts to eliminate greenwashing from the investment sector. End of an era I – The fight against greenwashing inched ahead with the release of final guidelines for naming ESG- or sustainability-related funds by the European Securities and Markets Authority (ESMA).

Market participants flag importance of double materiality to enhance Article 8/9 definition alignment, stress need to recognise transition strategies. Risk of uncertainty French asset manager Mirova’s response said the current definition of Article 8 products is “too broad”, while the definition of Article 9 is “too narrow”.

It remains to be seen whether the FCA insists that firms link gaps with the requirements to prevent harm under this year’s consumer duty measures, and require firms to provide adequate evidence to indicate proper due diligence in avoiding intentional greenwashing.

The EU Green Taxonomy was designed to accelerate the flow of money into green companies and projects, while simultaneously protecting investors from greenwashing accusations.

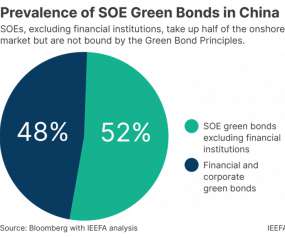

A key amendment requires 100% of the proceeds to fund green projects, instead of 50-70% previously. This is a big step for foreign investors who are eager to invest in China’s domestic green bond market but have concerns about greenwashing—inadvertently buying ‘green’ bonds that, in fact, support non-green projects.

It will also intensify its work on the effects of transition funding, greeninvestment needs and transition plans, exploring the case for further changes to its monetary policy instruments and portfolios. These announcements followed the ECB’s third assessment of European banks’ progress on the disclosure of climate and environmental risks. “So

The move towards net zero commitments has been facilitated by a “definite shift” by institutional investors in Asia toward use of international frameworks that provide a pathway to implementing commitments across portfolios.

The question is how stringent Indonesia should set the transition criteria, taking into account a pressing need to not only avoid charges of greenwashing or ‘transition washing’, but also build confidence in the country’s decarbonisation pathway. What is missing is a lack of clarity over what Indonesia considers transition activities.

Levick also noted that the taxonomy could be employed via initiatives such as a net zero test, which the UK might apply to all its public investment decisions, utilising the taxonomy to evaluate whether investments align with the its definition of ‘green’.

ING Asset Management’s new SDG Impact Strategy will provide clients with exposure to companies that contribute specifically to the 17 UN Sustainable Development Goals (SDGs), responding to strong demand for ‘dark green’ investments.

Currently, there is no clear definition of what constitutes a “green” investment, which has led to a proliferation of green bonds that are not truly environmentally friendly.” ChinaSIF estimates that the size of China’s ESG market in 2022 was RMB 24.6 trillion (US$3.57 trillion) growing from RMB 18.4 trillion in 2021.

trillion, prompting industry insiders to express doubt about how such a huge run-up could happen without greenwashing. This was triggered in part by stiff anti-greenwashing proposals from the U.S. European asset managers struck US$140 billion from ‘dark green’ investment category. greeninvestment.

There is also a lack of universally clear definitions surrounding sustainability risks, impacts and materiality. As the UK government also grapples with strengthening the economy, and the implementation of Brexit continues to rumble in the background, greeninvestment is naturally becoming deprioritised. of GDP from April 2027.

At issue is the practice of greenwashing, in which dubious or over-stated claims are made for the environmental or social impact of green-labelled funds and other financial products. The lack of any agreed definitions has made life difficult for both institutional and retail investors seeking genuine ESG products.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content