This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Paris-area public transport authority le-de-France Mobilits announced that it has raised 1 billion in a new greenbond offering, the first by a public entity to be issued under the European GreenBond (EuGB) Regulation.

The government of Australia will issue its first ever greenbond next year, joining the growing ranks of sovereign debt issuers participating in the sustainable finance market to help fund their environmental sustainability initiatives, according to an announcement on Friday by Treasurer Jim Chalmers.

million pounds of plastic from flights; KKR, ECP to invest $50 billion in datacenter capacity and power generation; law firms ramp up ESG training for lawyers; capital raises for sustainable heating, industrial decarbonization, energy sector emissions solutions, and more. Copper Mine Operations to Renewable Diesel Southwest Airlines Eliminates 1.5

Linklaters forecasts record year for greenbonds, while SLB issuance suffers Q2 slowdown. Investor demand for green, social, sustainability, sustainability-linked and transition bonds (GSS+) has surged in H1 2023, with regulatory developments bringing greater transparency and confidence to the market.

Lawmakers in the European Parliament voted 418-79 on Thursday to approve the adoption of a new European GreenBond (EuGB) label, aimed at fighting greenwashing and providing investors with confidence that their investments are being appropriately directed towards financing sustainable business activities and technologies.

Global issuance of labelled sustainable bonds including green, social, sustainability, sustainability-linked, and transition bonds is anticipated to again reach around $1 trillion in 2025, according to a new forecast released by Moodys Ratings, as headwinds including political changes from the new U.S.

As companies respond to demands for both mandatory and voluntary ESG disclosures, the risk of greenwashing grows. Investors and customers are also initiating litigation to hold companies accountable for greenwashing. Why evaluate greenwashing risks? Recent studies highlight how prevalent greenwashing has become.

Out of its class A secured debt of £15 billion, about £3 billion is labelled green, potentially making the company a greenbond default case. Greenbonds are structurally no different to conventional bonds under the same class (with the same ranking, covenants and security package among all creditors in the case of distress).

Corporate interest in sustainability-linked loans has grown rapidly over the past several years, as the financing provides flexibility to use proceeds for general corporate purposes, while with instruments such as greenbonds, raised funds can only be allocated to specific categories of green projects.

ESG finance is growing in importance precisely because it makes a key contribution to achieving these goals toward more sustainable development models. An interesting ongoing trend is the growth of greenbonds. In 2022, greenbond issues accounted for more than half of all sustainable bonds issued in the same year (58%, $487.1

trillion of bonds issued by the fossil fuel sector. They should also develop disclosure requirements of core complementary metrics for financial institutions and consider the impacts of existing policies on climate goals. trillion, compared with US$1.7

The pullback threatens to erode years of progress, which has made Europe the leading market for sustainable funds , greenbonds and other responsible investments, and jeopardizes the capital needed for the EUs ambitious climate goals. We need to treat these developments as a call to action. and Europe over the Ukraine war.

They in fact have no common yardstick to measure “sustainable” and are instead responding to general environmental and social concerns in the market with a range of instruments such as greenbonds and sustainability-linked loans that pay a bit of lip service to these issues while making money for the banks.

Issuance volumes of green, social, sustainability and sustainability-linked (GSSS) bonds rebounded strongly in Q1 2023, resuming double-digit growth trends after falling 18% in 2022, according to a new report from Moody’s Investors Service. Non-financial corporate issuance in the U.S.

Many investors are already familiar with greenbonds, which have been on the market since 2007. Greenbonds finance a specific project or projects with an environmentally beneficial purpose. Since then, companies have issued new types of bonds to finance a range of green, social and sustainable projects (Display).

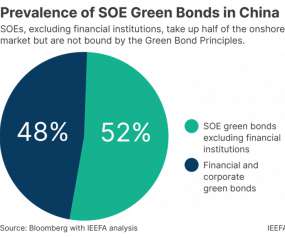

The IEEFA’s Christina Ng says China’s state-owned enterprises continue to allocate up to half of their greenbond proceeds to non-green projects. . China’s ambition to green its financial market has been making significant progress. SOEs accounted for about half the onshore green issuances from 2019 to 2022.

Originally published on bloomberg.com Green finance regulatory developments The 2023 United Nations Climate Change Conference (COP28) galvanized the energy around the global green finance agenda, setting the stage for a busy 2024 of green-related rulemaking and policy guidance for the financial services sector.

The answer depends on the fund, the region, the sector, and the company. In a market that expanded before firm regulatory guardrails were put in place, there is very valid concern that some transition-labelled funds may be perpetuating greenwashing by investing in companies misaligned with credible decarbonisation pathways.

In this paper, we describe our process for assessing ESG-labeled bonds and show that, by systematically applying this framework, investors can help set a gold standard for the market, avoid surprises from controversy and greenwashing, and potentially generate more alpha over time. Bigger, Broader, Better: The Rise of ESG-Labeled Bonds.

Moody’s anticipates that volumes may bottom out in the region in 2024, with tailwinds from incentives from the Inflation Reduction Act driving increases in green technologies, although the report also notes uncertainty from the upcoming U.S. election on federal climate policy clouding the issuance outlook.

This week in ESG news: EU adopts new law against greenwashing; Walmart reaches 1 billion ton supply chain emissions reduction milestone; S&P forecasts $1 trillion sustainable bond market in 2024; Airbus, TotalEnergies launch sustainable aviation fuel partnership; Verizon invests $1 billion in renewable energy; EU lawmakers agree to certification (..)

This week in ESG news: EY, Microsoft launch green skills training program; KPMG survey finds three quarters of companies not ready for upcoming ESG assurance requirements; BlackRock’s new climate transition-focused private debt fund; Austrian Airlines found guilty in greenwashing case; asset owners continuing to increase allocations to ESG investments (..)

In an oversubscribed market, greater opportunities for investors lie in social, sustainable, SLBs and blue bonds. Investor demand for green, social, sustainable, sustainability-linked and transition bonds (GSS+) is far outstripping supply, the Climate Bonds Initiative’s (CBI) GreenBond Pricing in the Primary Market H2 report illustrates.

Similarly to greenbonds, SLBs have also been criticised for acting as a potential ‘ platform for greenwashing ‘ , with their proceeds sometimes not being used for sustainable causes. Nevertheless, the flexibility they afford has been welcomed in some regions – particularly in developing markets. “We billion (US$8.5

In order to establish its central role, ESMA recommended completing the Taxonomy to cover all the economic activities that could substantially contribute to the EU environmental objectives, be extended to cover transition activities, and that a social taxonomy be developed. Click here to access the ESMA recommendations.

Mandatory EU GreenBond Standard risks slowing issuance, but voluntary approach can still drive Taxonomy-aligned volumes. On the face of it, the market for greenbonds is heading in the right direction, and fast.

Target-Based: ESG Bond Goals Have Expanded ESG-labeled bonds have come a long way quickly, and innovation shows no signs of slowing. UOPs, which are project-based, include greenbonds and social bonds that firms issue to finance their environmental or social programs.

Developed countries have belatedly reached a target for climate finance, only to be set a new one for nature. Developed nations mobilised US$115.9 billion of climate finance for developing countries in 2022, it was revealed this week, exceeding for the first time the US$100 billion annual level set in Copenhagen in 2009.

European regulators have ratcheted up efforts to eliminate greenwashing from the investment sector. End of an era I – The fight against greenwashing inched ahead with the release of final guidelines for naming ESG- or sustainability-related funds by the European Securities and Markets Authority (ESMA).

The Africa Development Bank estimates that the continent will require an average of US$1.4 The effects of this impasse are already becoming apparent; the World Bank estimates Africa has less than 1% of global greenbond issuances and pays more than twice than similarly rated peers to access markets. Time to commit.

Sovereigns have been relatively late entrants to sustainable bond markets following corporates and supra-national entities (such as the World Bank and the European Bank for Reconstruction and Development), which issued the first green debt securities in the mid-2000s.

Before developing a plan, most advisors will ask clients to think about their risk preferences, timelines, return expectations, and go-forward financial needs. Issuance of greenbonds has more than tripled from 2017 to 2021. What’s Your Goal? Traditionally, most experts in finance and economics thought this was an impossibility.

Moody’s cited challenges including short-term post-pandemic support for businesses and households, long-term sustainable development challenges, including climate risk mitigation, and gradual, uneven recovery in revenue streams. Developing economies globally need to invest as much as US$4.5 trillion) to reach the goals.

No country in the region has made reporting against the frameworks mandatory, further increasing greenwashing risk and due diligence costs. A comprehensive taxonomy can mitigate the risk of greenwashing by enforcing stringent requirements and maintaining transparency.”

No country in the region has made reporting against the frameworks mandatory, further increasing greenwashing risk and due diligence costs. A comprehensive taxonomy can mitigate the risk of greenwashing by enforcing stringent requirements and maintaining transparency.”

The rules were issued for consultation in January 2022, with the aim to enhance the transparency of disclosures on sustainability-related products, improve product comparability, and guard against greenwashing. . It must also appropriately reflect this focus in its investment objectives or strategy in its registration statement. .

In 2020, the largest sub-category in the climate funds market was clean energy/tech, which slipped to third last year ahead of low carbon and greenbond funds. . Morningstar said the shifts seen in 2021 reflected growing investor interest in opportunities beyond the renewable energy sector. .

billion tonnes of CO2 every year, as well as the packaging industry to develop alternatives to plastic. . Financial returns and greenbonds . Investors that choose the less fashionable option will also avoid paying a ‘greenium’ on already green companies – an issue that is particularly apparent in the world of greenbonds.

To support emerging market climate transitions, developed countries and private investors are drawing up an ambitious blueprint, but is it working? This JETP has been followed by new partnerships between developed countries and Indonesia , Vietnam and Senegal. gigatonnes of carbon emissions over the next 20 years.

Ashok Parameswaran, President of the Emerging Markets Investors Alliance, highlights the challenges of achieving environmental and social impact via emerging markets bonds. trillion by September, with demand for emerging market labelled bonds far outstripping the rest of the world. Weak frameworks. Gold standard.

Some fixed-income funds may purchase greenbonds issued by fossil fuel companies to help them finance renewable energy projects. A lot of the claims of “greenwashing” really have to do with a mismatch between investor expectations and a fund’s specific sustainable-investing approach. investors.

Further complicating matters, sustainable investing has not sprung forth as a unified, fully developed investment approach. As a result, much of the criticism stems from a mismatch between what a critic thinks sustainable investing is or should be about and how it is actually being practiced, often leading to claims of “greenwashing.”

EFAMA Senior Economist Vera Jotanovic said the supply and demand drivers of sustainable bond fund inflows were being supported by regulatory developments, notably the introduction of the Sustainable Finance Disclosures Regulation (SFDR) and the EU Taxonomy.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content