This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When I led Canada’s Social Investment Organization (SIO) in the early 2000s, one of our most important debates concerned the question of whether the organization should develop an industry-wide label for socially responsible investment, as sustainable investing was called back then.

The US SIF says this more cautious approach was at least partly triggered by recent US Securities and Exchange Commission (SEC) proposals to crack down on greenwashing by ramping up standards on the names and disclosure requirements for ESG funds. ESG] asset levels will likely move lower to a truer base of real sustainable investing.”.

These new rules, intended to counteract greenwashing, spell out the criteria for a greeninvestment and require market participants to disclose how they are aligned with them. The outcome is a seamless approach to customized sustainable investing. Media Contact: Arleta Majoch, COO Impact Cubed Arleta@impact-cubed.com.

Global issuance of labelled sustainable bonds including green, social, sustainability, sustainability-linked, and transition bonds is anticipated to again reach around $1 trillion in 2025, according to a new forecast released by Moodys Ratings, as headwinds including political changes from the new U.S.

We need to treat these developments as a call to action. European Commission announces clean industrial deal The EC also announced a clean industrial deal, a plan to encourage high-emitting industries like steel and cement to move toward a net-zero future and incentives for cleantech firms to expand greeninvestments.

BRUSSELS (AP) — The European Union on February 2 proposed including nuclear energy and natural gas in its plans for building a climate-friendly future, dividing member countries and drawing outcry from environmentalists as “greenwashing.” This anti-science plan represents the biggest greenwashing exercise of all time.

The European Union, China, the United Kingdom and about 20 other countries are developing such taxonomies as a way of discouraging greenwashing and channelling investment to the climate transition. The EU’s taxonomy has been particularly controversial because of its inclusion of natural gas and nuclear as “greeninvestments.”

Chinese asset managers are improving ESG awareness, but weak regulation means green claims often don’t match reality, says Greenpeace. Greenwashing is a growing risk in the Chinese fund management sector, as marketing of ESG products runs ahead of standards and regulatory oversight, a new report by Greenpeace has found.

The newly launched international initiative Taskforce on Nature-related Financial Disclosures is developing a risk management and disclosure framework for organizations to report and act on evolving nature-related financial risks. We need to encourage more targeted investments in nature-positive solutions that reverse biodiversity loss.

Investors have been in limbo for six months about the future of the regulation, which provides guidelines on the disclosures required of greeninvestment vehicles. Therefore, replacing this current framework with actual categories with clear criteria is a possibility.

Asset managers decide to re-label existing funds as greeninvestment vehicles for two reasons, according to Paul Lacroix, Head of Structuring at Smart Beta specialist investment firm Ossiam, an affiliate of Natixis. The first is client demand for investment solutions that are ESG-based,” he tells ESG Investor.

EU markets regulator the European Securities and Markets Authority (ESMA) released its finalized guidelines on ESG Funds’ Names earlier this year, aimed at protecting investors from greenwashing risk, and detailing minimum standards and thresholds for funds using ESG and sustainability-related terms in their names.

European regulators have ratcheted up efforts to eliminate greenwashing from the investment sector. End of an era I – The fight against greenwashing inched ahead with the release of final guidelines for naming ESG- or sustainability-related funds by the European Securities and Markets Authority (ESMA).

Negligible impact on SDGs – The need to close a massive financing gap to achieve the UN Sustainable Development Goals (SDGs) is well established. Regulators are already pushing back against the risk of greenwashing with a range of fund disclosure , naming and labelling rules. billion) greeninvestment pledge.

It was supported by an informal technical expert group, and a founding partner group consisting of Global Canopy, UNDP, UNEP FI, and WWF, to develop recommendations for more effective nature-related disclosures in order to promote more informed investment decision-making.

Talks, then action – With just 15% of the Sustainable Development Goals on track, this week’s UN SDG Summit saw governments rally behind a political declaration that emphasised the need to close a yawning finance gap. Anti-greenwashing action returned on both sides of the Atlantic this week. What’s in a name?

Inclusion of coal in green taxonomy would border on state-sanctioned greenwashing, says Christina Ng, Research & Stakeholder Engagement Leader, Debt Markets, and Putra Adhiguana, Energy Technologies Research Lead, Asia, at IEEFA. A huge controversy erupted last year when the EU labeled gas power plants as sustainable.

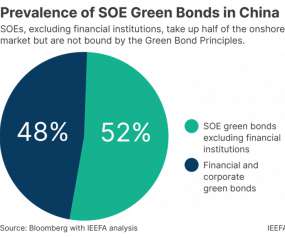

A key amendment requires 100% of the proceeds to fund green projects, instead of 50-70% previously. This is a big step for foreign investors who are eager to invest in China’s domestic green bond market but have concerns about greenwashing—inadvertently buying ‘green’ bonds that, in fact, support non-green projects.

In fact, 41 out of the 47 taxonomies currently under development have either stated outright or implied that they aim for their respective taxonomies to be used to guide policymakers and authorities, or they are in the early stages of development and have yet to make such an intention clear.

“Most banks’ fossil fuel policies focus on a small portion of their financing – the direct financing of new oil and gas assets – and fail to capture the vast streams of capital going to companies developing these assets.

However, green bond issuances are often associated with investment-grade issuers of relatively low credit risk: developed countries, development banks, large financial institutions and corporates (they are often more likely to have the resources to develop a green bond framework and execute a portfolio of green assets).

There have been bad faith actors from the corporate world, greenwashing their activities, depleting the world’s resources, damaging the environment and wasting the planet’s and the climate movement’s time and energies. Many people are cautious about the intentions of companies that have committed to decarbonization and with some reason.

ING Asset Management’s new SDG Impact Strategy will provide clients with exposure to companies that contribute specifically to the 17 UN Sustainable Development Goals (SDGs), responding to strong demand for ‘dark green’ investments. ING’s smallest investment strategy has €1 billion in AuM, while its largest manages €8 billion.

Rampant criticism of greeninvestment will only accelerate its maturity. In the two weeks since our last blog, and the three since the Financial Times’ Katie Martin first tweeted about Stuart Kirk’s fêted and ill-fated climate-risk speech, there’s been an avalanche of comment on the failings and misunderstandings of ESG investing.

The UK’s Financial Conduct Authority (FCA) will closely monitor funds’ use of incoming greeninvestment labels, potentially stopping asset managers from using them in the event of misuse. . Regulator’s ESG head underlines need for market confidence, highlights importance of investor engagement. .

Levick also gave oral evidence, noting her additional role as Co-Head of the UK’s Transition Plan Taskforce (TPT) Secretariat, a group launched by HM Treasury to develop a framework for companies to disclose their climate transition plans, which is expected to eventually be made mandatory by the UK government.

The question is how stringent Indonesia should set the transition criteria, taking into account a pressing need to not only avoid charges of greenwashing or ‘transition washing’, but also build confidence in the country’s decarbonisation pathway.

The intention is that this should help both the firms’ institutional clients (such as pension scheme trustees) and ‘end-user’ consumers (such as scheme members or retail investors) to more easily identify so-called greeninvestments and direct their funds accordingly.

While this may be true for traditional long-only markets (not withstanding that different time periods may lead to wildly different results), the question becomes a lot more complex when investing to manage environmental, social or governance (ESG) risks or to achieve UN Sustainable Development Goals (SDGs). Creating confusion.

Not least plans for a ‘loss and damage’ fund, which aims to help the most climate-vulnerable emerging markets and developing economies (EMDEs) cover the costs of climate change’s physical impacts. The launch of the FCLP is the most important development in relation to sustainable use of nature.

For insurance companies it means they need to consider ESG and green finance issues when selling their insurance products and consider it in their asset management arm as well.” ChinaSIF estimates that the size of China’s ESG market in 2022 was RMB 24.6 trillion (US$3.57 trillion) growing from RMB 18.4 trillion in 2021.

Meeting in Sapporo, Japan, Group of Seven climate ministers on Sunday committed to updating their National Biodiversity Strategy and Action Plans to meet the objectives of the Global Biodiversity Framework and supporting the development of national biodiversity finance plans for all signatories.

trillion, prompting industry insiders to express doubt about how such a huge run-up could happen without greenwashing. This was triggered in part by stiff anti-greenwashing proposals from the U.S. European asset managers struck US$140 billion from ‘dark green’ investment category. greeninvestment.

The government of the small west African nation switched existing debt for a US$500 million ‘ blue bond ’ with a lower rate and a longer maturity, with the intention of generating US$163 million for marine conservation; the US Development Finance Corporation provided the risk insurance that secured its Aa2 credit rating.

While the intention of the EUGBS is to improve standards and reduce the risk of greenwashing is admirable, the reality is its limited scope, he adds. Its prescriptive nature and rigidity, could inadvertently create friction, thus stifling the development of the sustainable debt market.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content