This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This turnabout has been most pronounced in the greenbond market, where power utilities have, controversially, been adding nuclear energy as an option for greenbonds. With this in mind, nuclear greenbonds promise to help fund decades of net-zero energy for the public and years of clean financial returns for investors.

A 2020 report co-authored by Amundi and the IFC pointed out that investment flows since the start of the COVID-19 crisis have proven more resilient towards greeninvestments when compared to their traditional counterparts. What is the potential of greenbonds to address this imbalance?

While 2024 issuance remained flat year-over-year at $1 trillion, however, sustainable bond volumes underperformed strong growth in the overall bond market in the year, with share of global issuance declining to 11% from 15% in the prior year.

Out of its class A secured debt of £15 billion, about £3 billion is labelled green, potentially making the company a greenbond default case. Greenbonds are structurally no different to conventional bonds under the same class (with the same ranking, covenants and security package among all creditors in the case of distress).

Outstanding green loans stood at 908 billion in 2023 while greenbond volumes reached 781 billion. Total outstanding green debt finance at the end of 2023 was 1.7

As the green-bond market matures, it is developing offshoots. The types of projects financed, as well as the emergence of innovative types of bonds and loans linked to the ESG targets, is growing. These initiatives may broaden the market for greeninvestment options.

The pullback threatens to erode years of progress, which has made Europe the leading market for sustainable funds , greenbonds and other responsible investments, and jeopardizes the capital needed for the EUs ambitious climate goals.

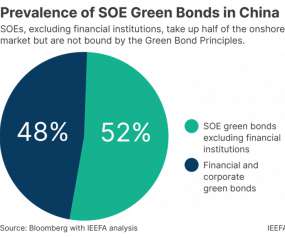

The IEEFA’s Christina Ng says China’s state-owned enterprises continue to allocate up to half of their greenbond proceeds to non-green projects. . China’s ambition to green its financial market has been making significant progress. SOEs accounted for about half the onshore green issuances from 2019 to 2022.

Cryptocurrencies have been condemned over their environmental record at a time when traditional investments have been rapidly moving towards greener environmental, social and governance (ESG) values. So how long will it be until crypto earns its green credentials?

Global media and communications company announced today its first greenbond offering, raising $1 billion, with proceeds from the 10-year bond aimed at supporting the company’s environmental sustainability goals, including its target to be carbon neutral by 2035. Ramirez & Company, Inc.,

By bond type, greenbonds continued to dominate the GSSS market at 60% of volumes, with issuance rising 26% quarter-over-quarter and 3% year-over-year to $169 billion, with strong performance from nonfinancial corporate issuers and sovereigns at $61 billion and $53 billion, respectively.

Green finance – typically global bond, loans, and other long-term markets – has reached almost US$2 trillion in volume. Annual greenbond issuance broke through the half trillion mark for the first time, ending 2021 at US$522.7 billion, a 75% increase on prior year volumes, according to the Climate Bonds Initiative.

Transition funds’ fossil fuel investments, however, were highly concentrated in “firms rated by ESG rating providers as environmental leaders within their sector, and with the potential to contribute to the EU’s environmental objectives,” and also tended to favor greenbonds issued by fossil fuels and utilities sector firms.

Issuance volume rose 45% over 2020, with sustainable bonds accounting for 10% of overall debt capital market activity. Greenbonds accounted for around half of all issuance (US$488.8 Social bond issues totalled US192.9 Q4 2021 was the fourth consecutive quarter to surpass US$200 billion and over 400 issues.

Achieving certification will help demonstrate alignment with the greenbond requirements of the Climate Bonds Initiative and the EU Taxonomy for Sustainable Investment, as well as with World Bank and IFC performance standards.

It had previously been possible to launch an EU environmental opportunities fund, claiming Article 8 classification under the Sustainable Finance Disclosure Regulation (SFDR) , while allocating as little as 10% of assets to demonstrably greeninvestments.

The EU Green Taxonomy is also instrumental for the upcoming EU GreenBonds Standard. As the cornerstone of many current and upcoming regulations, the quality and comparability of the EU Green Taxonomy’s reporting data is crucial.

Malaysia, for example, offers a GreenInvestment Tax Allowance on green assets for the owners of those assets and companies that undertake green technology projects, and a Green Income Tax Exemption for service providers, including a separate category for owners of solar photovoltaic systems.

The rise of taxonomies of sustainable activities reflects a recognition from policymakers that global financial markets depend on a shared classification system if they are to identify ‘green’ investment opportunities.

Impakter How the European Central Bank’s New Climate Policy Could Reduce Both Emissions and Inflation More often than not, conversations on the economy engender a somewhat inanimate, two-dimensional and transactional impression, but in truth, the economy is defined by more than just balance sheets, the stock exchange, trade, or investment.

As sukuk are linked to assets that may be eligible for green and social projects, they will become vital tools to fund the UN SDGs,” said Shrey Kohli, Director, Head of Debt Capital Markets, London Stock Exchange, and Chair of the HLWG on Green and Sustainability Sukuk. Future growth potential in Gulf.

NN IP Expands Impact Range with New Social Bond Fund. Billion GreenBond to Fund Ag and Value Chain Sustainability Projects. Iberdrola Signs $550 Million Green Loan with EIB to Fund Wind & Solar Projects. OPG Issues $300M “Nuclear GreenBond”. Sustainable Finance. PepsiCo Issues $1.25 Exec Moves.

Currently, there is no clear definition of what constitutes a “green” investment, which has led to a proliferation of greenbonds that are not truly environmentally friendly.” Hewett says a key challenge for China’s sustainable finance sector is a lack of unified standards and regulations.

This week, green and blue debt were in focus around the world, while the US courted further climate controversy. New peaks – Greenbonds and other sustainability-related instruments demonstrated their resilience this week. The act also kickstarted an era of greeninvestment competition.

After years of debate, the European Union GreenBond Standard (EUGBS) finally made its formal debut at the end of last year. However, all of the projects must comply with the taxonomys do no significant harm (DNSH) criteria, as well as be certified by a designated EU greenbond reviewer.

The takeaway : Expect sustainable mutual fund and ETF inflows to bottom out in 2025 and investors to return to these products, as long-term interest rates improve conditions for greenbonds and climate-friendly stocks and European investors become more familiar with ESG fund-disclosure rules.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content