This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

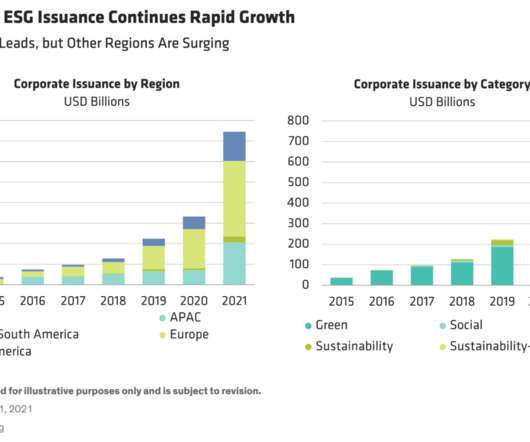

ESG-labeled bond issuance surged to new heights in 2021. Greenbonds, which fund particular projects, continued to dominate. But issuance of social, sustainability and sustainability-linked bonds—which reference specific key performance indicators, or KPIs—grew fastest (Display).

Indeed, sustainable investments are key to building a society that is low-emission , keeping global warming below 2°, and socially inclusive. An interesting ongoing trend is the growth of greenbonds. In 2022, greenbond issues accounted for more than half of all sustainablebonds issued in the same year (58%, $487.1

David Zahn , Head of Sustainable Fixed Income at Franklin Templeton , says new standards and innovations are expanding the supply of greenbonds to meet increased investor demand. Investor demand for green, social, sustainability-linked and transition bonds (GSS+) continues to rise rapidly, outstripping supply.

Despite development barriers, opportunities are emerging for investment in sustainable assets in growing market. Africa has seen rapid growth in issuance of green, social, sustainability and sustainability-linked (GSS+) bonds and could prove enticing to investors, in spite of existing challenges.

Sovereigns have been relatively late entrants to sustainablebond markets following corporates and supra-national entities (such as the World Bank and the European Bank for Reconstruction and Development), which issued the first green debt securities in the mid-2000s.

Benchmarked against the iBoxx Global Green, Social, Sustainability index, it will be assessed at the issuer level for both ESG-labelled debt, including sustainablebonds, and non-labelled debt. The fight against climate change has driven strong growth momentum in the global greenbond market.

Yet, establishing robust E&S frameworks to ensure land-use investments create positive impacts and avoid harms is a complex matter, with the physical scale, often geographically remote nature and novelty of such deals all presenting challenges to corporates, agri lenders and investors.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content