This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

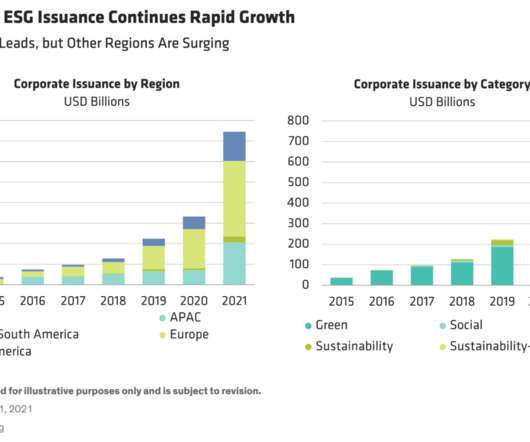

ESG-labeled bond issuance surged to new heights in 2021. Greenbonds, which fund particular projects, continued to dominate. But issuance of social, sustainability and sustainability-linked bonds—which reference specific key performance indicators, or KPIs—grew fastest (Display).

The Government of India will issue its first-ever greenbond this month, according to an announcement by the Reserve Bank of India, with plans to raise approximately US$2 billion to support green infrastructure projects aimed at reducing the carbon intensity of the economy. Last week, the government of Hong Kong raised US$5.8

The Government of Hong Kong announced today the completion of a greenbond issuance, raising $5.75 billion in a triple-currency offering, with bonds denominated in US dollars, Euros and Renminbi (RMB). According to the Hong Kong Monetary Authority, the offering marks the largest ESG bond issuance in Asia to date.

Linklaters forecasts record year for greenbonds, while SLB issuance suffers Q2 slowdown. Investor demand for green, social, sustainability, sustainability-linked and transition bonds (GSS+) has surged in H1 2023, with regulatory developments bringing greater transparency and confidence to the market.

Global issuance of labelled sustainablebonds including green, social, sustainability, sustainability-linked, and transition bonds is anticipated to again reach around $1 trillion in 2025, according to a new forecast released by Moodys Ratings, as headwinds including political changes from the new U.S.

The recent EU directive on sustainability reporting – Corporate Sustainability Reporting Directive (CSRD) – also aims for transparency to improve sustainability reporting and to recognize the natural connection between ESG results and those reported in traditional statutory financial statements.

Asset managers Head of Fixed Income hopes market expansion will eliminate need for the purely greenbond-focused vehicle within the next decade. Niche to mainstream evolution Storebrand stated that the fund was the first commercial greenbond fund, building on the first ever greenbond issued by the World Bank in 2008.

Issuance volumes of green, social, sustainability and sustainability-linked (GSSS) bonds rebounded strongly in Q1 2023, resuming double-digit growth trends after falling 18% in 2022, according to a new report from Moody’s Investors Service. Non-financial corporate issuance in the U.S.

Originally published on bloomberg.com Bloomberg announced the launch of new green-tilted fixed income indices, which seek to increase weighting to greenbonds in some of Bloomberg’s flagship indices such as the Global Aggregate, Treasury and Corporate Indices.

David Zahn , Head of Sustainable Fixed Income at Franklin Templeton , says new standards and innovations are expanding the supply of greenbonds to meet increased investor demand. Investor demand for green, social, sustainability-linked and transition bonds (GSS+) continues to rise rapidly, outstripping supply.

Sustainablebond issuance outperformed the broader market in the second quarter of 2022, reaching a record 15% of global total issuance, according to a new report from Moody’s ESG Solutions. Moody’s maintained its forecast for stronger GSSS volumes in the second half of the year, and its $1 trillion full year estimate.

Indeed, sustainable investments are key to building a society that is low-emission , keeping global warming below 2°, and socially inclusive. An interesting ongoing trend is the growth of greenbonds. In 2022, greenbond issues accounted for more than half of all sustainablebonds issued in the same year (58%, $487.1

Global issuance of labelled sustainablebonds – including green, social, sustainability, sustainability-linked, and transition bonds – declined sharply in the second quarter of 2024, as fewer new issuers entered the market and issuers contend with regulatory scrutiny, according to a new report released by Moody’s Ratings.

Issuances of green, social, sustainability and sustainability-linked (GSSS) bonds fell in the third quarter of 2022, but continued to remain more resilient than the broader bond market, growing to a record 16% share of the market in the quarter, according to a new report from Moody’s Investors Service.

The Securities and Exchange Board of India (SEBI) is considering expanding its greenbond framework to include social, sustainability and sustainability-linked fixed income instruments and securitised debt.

Issuance volumes of green, social, sustainability and sustainability-linked (GSSS) bonds rebounded sharply in Q1 2024 over the prior quarter, rising 36% to $281 billion, up from $207 billion in Q4 2023, according to a new report from Moody’s Investors Service.

Shades of Green’s Second Party Opinions (SPOs) are independent, research-based assessments on companies’ and governments’ green, sustainability and sustainability-linked debt issuances and frameworks, evaluating alignment with market standards, typically provided before any borrowing is raised. trillion 2 years ago.

In addition to volume growth, S&P also anticipates an expansion in bond types, with a more prominent presence for transition and blue bonds, even as greenbonds continue to dominate. For 2024, the report forecasts GSSSB issuance volumes of $0.95 trillion to $1.05 trillion, growing slightly from $0.98

The launch of the new funds follows several years of significant growth in the sustainablebond market, as companies and governments have turned to sustainablebonds to help finance their climate, environmental and social commitments and initiatives.

Moody’s anticipates that volumes may bottom out in the region in 2024, with tailwinds from incentives from the Inflation Reduction Act driving increases in green technologies, although the report also notes uncertainty from the upcoming U.S. election on federal climate policy clouding the issuance outlook.

The quarter also saw a continued divergence in regional GSSS trends, with sustainablebond volumes representing 19% of total bond issuance in Europe year-to-date, compared to only 4.5% Despite the pullback, Moody’s maintained its full year forecast for greenbond issuance of $550 billion, up more than 10% over 2022.

In a post announcing the new issuance, Deutsche Bank said: “With this milestone, we expand our ESG issuance programme, which began in 2020 with our first greenbond issuance.

Aeroporti di Roma (ADR), the manager and developer of Rome Fiumicino and Ciampino airports, announced the completion of a new 10-year €400 million sustainability-linked bond (SLB), with the cost of debt on the bond tied to a series of the airport operations group’s climate-related goals.

For the second quarter, GSSS bond issuance volumes of $258 billion were flat over the same period last year, recovering from a sharp decline in the second half of 2022, and significantly outperforming the broader market, with GSSS bonds rising to 15% share of global bond market issuance.

In an oversubscribed market, greater opportunities for investors lie in social, sustainable, SLBs and blue bonds. Thematic bonds have issuers and investors head over heels for one another ! In the GSS+ bond market, greenbonds are the most established label and account for over half of labelled volumes.

The sustainable finance indicators track the issuance and holdings of debt instruments with sustainability characteristics, such as green, social, sustainability and sustainability-linked bonds in the euro area, providing information on the proceeds raised to finance sustainable projects.

Issuance volumes for SLBs were particularly weak in the second half of the year, as issuers faced scrutiny of the credibility and robustness of their linked sustainability targets, as well as the sector’s exposure to high-yield issuance.

Green, social, sustainability, sustainability-linked and transition ( GSS+ ) bonds are shaking off recent macroeconomic and geopolitical volatility, with the market on track to hit US$5 trillion in combined issuance by the end of the year. Greenbonds made up 62% of the total aligned GSS+ debt (US$278.8

Ujala Qadir, Director of Strategic Programmes at the Climate Bonds Initiative, explains why the organisation has expanded its greenbond taxonomy to cover climate resilience. The market has matured as investors, issuers and other market participants have become more familiar with labelled debt,” she told ESG Investor.

Climate Bonds’ newly released annual report highlighted the discrepancy in greenbond issuance volumes between developing and emerging markets last year. . Three quarters (73%) of greenbond issuance originated from developed markets (DM), while 21% came from EMs. trillion, the Climate Bonds report said.

For the report, Sustainable Fitch examined the green, social, sustainability and sustainability-linked labeled bonds rated by its ESG Ratings service, with a focus on the instruments’ Use of Proceeds’ contribution to green and social impact, and the level of transparency and ambition in project or target selection.

Climate Bonds Initiative’s (CBI) Market Intelligence report found green, social, sustainability, sustainability-linked (SLB) and transition bonds (collectively known as GSS+) had fallen from over a record US$1 trillion in 2021 to US$863.4 Of that total, sustainabilitybonds contributed US$166.4

Despite development barriers, opportunities are emerging for investment in sustainable assets in growing market. Africa has seen rapid growth in issuance of green, social, sustainability and sustainability-linked (GSS+) bonds and could prove enticing to investors, in spite of existing challenges.

Achieving net zero by 2050 could require the climate bond universe to reach US$36 trillion by 2025 and over US$60 trillion by 2030, it added. The ESG-labelled bond markets are typically considered to include green, social, sustainability, sustainability-linked and transition bonds.

While it’s interesting to note that 18 WFE members report their Scope 3 emissions, more material is their role in supporting the sustainability strategies of investors. In that respect, the picture is still somewhat mixed.

Socialsustainability requires considering their needs. There’s a need for examples of organizations with “successful social justice strategies and processes,” wrote a North American academic. Get Started: What Is SocialSustainability provides an overall framework for action. Sustainable Finance 10.

Sovereigns have been relatively late entrants to sustainablebond markets following corporates and supra-national entities (such as the World Bank and the European Bank for Reconstruction and Development), which issued the first green debt securities in the mid-2000s.

Sustainabilitybonds and loans achieve scale One of the greatest challenges for the impact ecosystem has been the creation of scalable instruments that can attract institutional investors into projects that create financial returns alongside environmental and societal benefits.

Our sustainable debt markets are designed to highlight sustainable investment opportunities to investors with a green, social or sustainable investment agenda. The number of sustainable debt instruments listed on Nasdaq grew by 11% during 2022 and the volume of listed bonds grew by 27%.

Global sustainablebond issuance surged in 2021, with data providers estimating total volumes just above or below US$1 trillion; greenbonds accounted for roughly half. trillion by the end of 2022. Transition challenges. But issuance by sovereigns will grow from a low base, especially in Asia.

Strategy looks to invest in issuers “actively” shifting towards renewables, environmentally sustainable practices. It will be available both as a SICAV – the JPMorgan Funds – GreenSocialSustainableBond Fund (SICAV), and as an ETF, the JPMorgan ETFs (Ireland) ICAV – GreenSocialSustainableBond UCITS ETF.

Benchmarked against the iBoxx Global Green, Social, Sustainability index, it will be assessed at the issuer level for both ESG-labelled debt, including sustainablebonds, and non-labelled debt. The fight against climate change has driven strong growth momentum in the global greenbond market.

The MS INVF Calvert Sustainable Climate Transition Fund and MS INVF Calvert Sustainable Global GreenBond Fund are two new Article 9-compliant Luxembourg-domiciled global responsible investing funds developed in partnership with Calvert Research and Management.

An important key to unlocking that finance lies in green and sustainable emerging market bonds, which promise lenders both returns and the opportunity to invest in projects with an ESG impact. EMIA lists recipients of the gold standard on its site.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content